The U.S. tax code is, in a word, enormous, in the way an elephant is enormous compared to an ant, or Mount Everest is enormous compared to the pile of leaves in your yard after a day of fall raking.

The King James Bible is about 800,000 words in length. Anyone who has ever read, or tried to read, the Bible from Genesis to Revelation understands the scope of that project. Depending on your source, the number of words in the U.S. tax code - and associated documents - varies by hundreds of thousands or even millions of words. When applying those associated documents, it can be tabbed at roughly four million words.

To put that in a different perspective:

- Four million minutes adds up to more than seven years.

- Four million inches is 63 miles.

- Four million miles would take us to the moon and back 8 times.

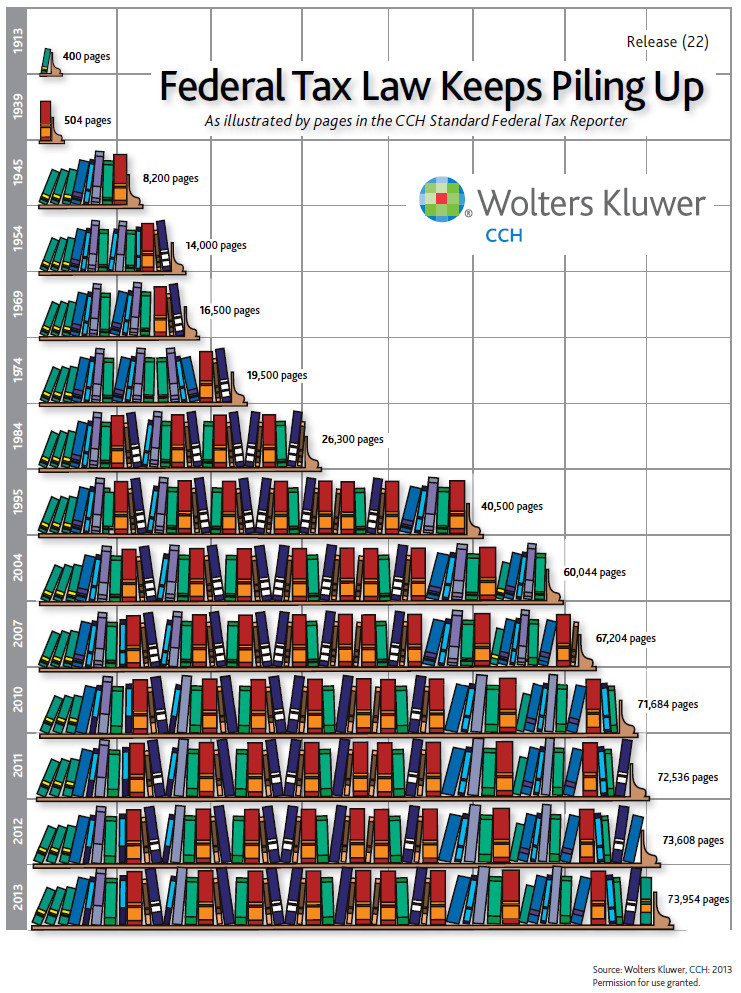

According to a diagram by Wolters Kluwer, in 1913, the year the income tax was inaugurated, the U.S. tax code was 400 pages long. In 1945, the year World War II ended, the code had added about 8,000 more pages. By 1984, the year of which George Orwell had warned us, the tax code had tripled, to about 26,000 pages.

{kind=link}

After that, it really starts to take off thanks to the Tax Reform Act of 1986. This law was enacted to simplify the tax code by closing loopholes and shutting down abusive tax shelters. Today this ever-expanding bane of paper-producing trees everywhere checks in at about 75,000 pages. So much for simplification.

How bad is it? Here are the opening paragraphs from the IRS’s “Tax Code, Regulations, and Official Guidance”:

“The version of the IRC underlying the retrieval functions presented above is generated from the official version of the U.S. Code made available to the public by Congress. However, this version is only current through the 1st Session of the 112th Congress convened in 2011. Before relying on an IRC section retrieved from this or any other publicly accessible version of the U.S. Code, please check the U.S. Code Classification Tables published by the U.S. House of Representatives to verify that there have been no amendments since that session of Congress.

“Finally, the IRC is complex and its sections must be read in the context of the entire Code and the court decisions that interpret it. At a minimum, please do not be misled by the false interpretations of the IRC promoted by the purveyors of anti-tax law evasion schemes.”

On such a scale, it is becoming – or has become – virtually impossible for a business of any size or complexity to, on its own, prepare an accurate tax return, one that does the best possible job of reducing tax liability and meeting all legal reporting requirements. Individual taxpayers with financial holdings above the most basic elements of income and savings are at a true and potentially serious disadvantage.

The challenge for everyone – particularly those in the financial planning and accounting fields – is to keep current on the code and its associated regulations, rulings, cases, bulletins, updates, and annual changes resulting from congressional changes in tax law. It’s fair to wonder how much bigger the code can become, and how much longer it will take, before its sheer weight causes it to collapse upon itself - or drives efforts to substantially reform the tax code?

The short answer is, not substantially bigger, and not indefinitely. But typically it takes a crisis to bring about change. There routinely are calls to reform, shorten, streamline, and make simpler the U.S. tax code. And those calls will continue to be made, routinely.

That crisis is out there, and coming closer all the time.

Share